One of the most important events in Financial Markets at present is the cessation of LIBOR.

The pound sterling, Euro, Swiss franc, Japanese yen LIBOR panel, and the one-week and two-month U.S. dollar LIBOR panel were phased out by the end of 2021, and the remaining U.S. dollar LIBOR tenors will cease by the end of June 2023. For the LIBOR index, the Secured Overnight Funding Rate (SOFR) has been identified and chosen as the preferred alternative and new benchmark replacement rate for U.S. dollar-denominated contracts.

Financial market participants need to start planning the transition of their existing portfolios, which reference LIBOR to avoid any issues once it is not published anymore. Existing derivatives’ transactions require a bilateral amendment to address IBOR indexes discontinuation adequately

Summit supports the transition of IBOR trades to RFR for individual trades from the respective trade application window and in “Bulk” mode using the RFR Bulk Transition utility.

It offers the following RFR Transition methods:

1. Terminate and Create New:

In this method, the IBOR indexed trade (Parent) is terminated, and a new trade (Child) is created with RFR Index. The RFR start date on the Child trade is, by default, the start date of the next interest period on the IBOR leg. The RFR start date can be modified such that the RFR effective date can be in the future. If transition needs to be applied with a future ASOF date, then the Terminate and Create New method should be used.

The supported trade types for RFR Transition Terminate and Create New approach are:

- Swap trades in single currency, Swap trades with notional exchange, interest rules and stubs set, Swap trades that have the same or different frequencies, Swap trades that have not yet started.

- Swap trades with different amortization types – fixed amortization, annuity amortization, fixed end amortization, customized amortization, variable amortization

- Partially terminated swap trades

- Swap trades with products or formulas

- Cross-currency swap trades, with or without products

- Money Market trades

- Commercial lending trades

- Floating to floating swap trades with a desynchronized schedule

- Floating to floating swap trades with a transferable index versus a non-transferable index

- Trades with payment frequency different than reset frequency

- Trades with customized flows

- Cap and floor trades

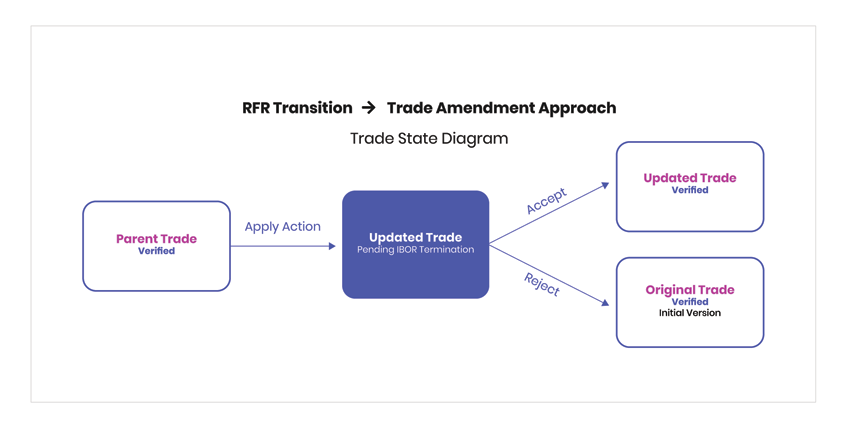

2. Standard Trade Amendment

The Trade Amendment method will modify the original IBOR trade. No new trade is created. The trade will have the RFR index applied for future periods. The limitation of the Trade amendment methodology is that it can be applied only for transition with an effective date as of the start of the next interest rate period. However, it cannot be applied for any future interest rate period as it requires all the future IBOR rate fixings to be applied now before RFR Effective date.

The supported trade types for RFR Transition using Trade Amendment approach are:

- Swap trades in single currency

- Swap trades with different amortization types – fixed amortization, annuity amortization, fixed end amortization, customized amortization, variable amortization, percentage and loan amortization

- Swap trades with products or formulas (Formulas like CCYSWAP, FLOAT_CAP_FLOOR, CMS_ADJ, CMS_BOSV, QUANTO, CMS, AVG, ABS, EXP, IF, LN, MAX, MIN, ROUND, SQRT, SUM)

- Money market trades

- Commercial lending trades

- Floating to floating swap trades with a desynchronized schedule

- Floating to floating swap trades with a term index versus an averaged index

- Floating to floating swap trades with a transferable index versus a non-transferable index

- Trades with payment frequency different than reset frequency

- Trades with customized flows

- Callable Swaps

- Swaption trades with CCYSWAP, FLOAT_CAP_FLOOR, CMS_ADJ, CMS_BOSV, QUANTO, CMS, AVG, ABS, EXP, IF, LN, MAX, MIN, ROUND, SQRT, SUM, REVFLOAT_F, PIECE_WISE product is supported

- European swaption trades and American swaption trades

- Swap trades with amortization and fees using BSGN or THWT models

- Exotic trades

Exotic trades with the following products or formulas – CCYSWAP, FLOAT_CAP_FLOOR, CMS_ADJ, CMS_BOSV, QUANTO, CMS, AVG, ABS, EXP, IF, LN, MAX, MIN, ROUND, SQRT, SUM, REVFLOAT_F, PIECE_WISE product is supported

3. CCP Terminate and Create New

The Terminate and Create New method has been extended to support the Central Counterparty Clearing Houses (CCP) Methodology.

The characteristics of the CCP methodology are:

- The RFR start date is considered the beginning of the current period (even if fixings are already done).

- The standard payment lag (2D) is used in the Child trade. This payment lag of 2D is inherited from the corresponding RFR Asset ID, set in RFR Transition Configuration Definition. The parent trade keeps the legacy lag (typically 0D).

4. ISDA Fallback Amendment with RFR Fixing Method as Rate Averaging

The International Swaps and Derivatives Association Inc. (ISDA) has published its 2020 IBOR Fallbacks Protocol and related Amendments to the 2006 ISDA Definitions to address the discontinuation of the U.S. dollar (USD) LIBOR and other interbank offered rates (IBORs) in the global derivatives market. For these trades, you can now compute the cashflows using the Dynamic Backward Shift method. In this method, you can reset past fixings by using the average rate, computed based on Summit observation.

5. ISDA Fallback Amendment with RFR Fixing Method asISDA Fallback

This method is similar to the earlier ISDA method, except that the ISDA Fallback rates are imported from external providers instead of calculating rates using rate averaging. The ISDA Fallback rates are stored in a separate table and need to be imported into the system before the rate reset process is run. Cashflows are computed using the Dynamic Backward Shift method.

Greenpoint Summit Team can help ….

GreenPoint is global partner with Finastra across multiple technology and services platforms. We have rich expertise in Summit migration and upgrade Including LIBOR transition.

- Experience in multiple versions of Summit (v5.x to v6.1, v6.2,v6.3) including RFR(Transition), UXP, SSO and Summit Training.

- GreenPoint Summit offers a comprehensive service encompassing new implementations, version and module upgrades, product and application development, test automation, cloud migration, and system maintenance

- Our quantitative services and platforms include Libor Replacement Simulation Tool (LRST), curve creation, recreation and management, model validation and documentation, and creation of challenger models for regulatory compliance.

- Our summit professionals also provide data porting, migration and management as well as cloud services.

- Over the last year we have completed several projects including full system upgrades, Libor/RFR migration, replacement of valuation frameworks, and custom code creation and testing for large global banks and insurers..